Blog

Article

Young doctors: Do you have adequate insurance coverage?

Author(s):

Why physicians need to understand and insure the gap between earning potential and net worth.

© Olivier Le Moal - stock.adobe.com

Young doctors and hospital administrators entering their careers face a myriad of financial decisions. One is determining how much insurance to secure. As important as disability and life insurance are, they may not always be a top priority for young doctors. This could lead to inadequate insurance coverage. Purchasing insurance in addition to that which is offered by an employer, such as life and long-term disability insurance, at the outset of a career can provide crucial financial protection and peace of mind for years to come.

Disability – more common than you may think

Jamie Malone, CFP®, CPA, CFA

© Agili

Many people drastically underestimate the likelihood of experiencing a long-term disability over the course of a career. As of January 2022, data from the Social Security Administration (SSA) suggests that about one in four of today's 20-year-olds will become disabled before they retire. Furthermore, the Council for Disability Awareness (CDA) reported that one in four of today's 20-year-olds can expect to be out of work for at least a year due to a disabling condition before they reach retirement age. Disability may be caused by accidents, of course, but also include long-term conditions and illnesses such as cancer, heart disease, back issues, etc. These statistics underline the importance of determining if one’s insurance coverage is sufficient. Given the high stress environment of health care settings and the physical demands of providing medical care, doctors should be thoughtful about insurance.

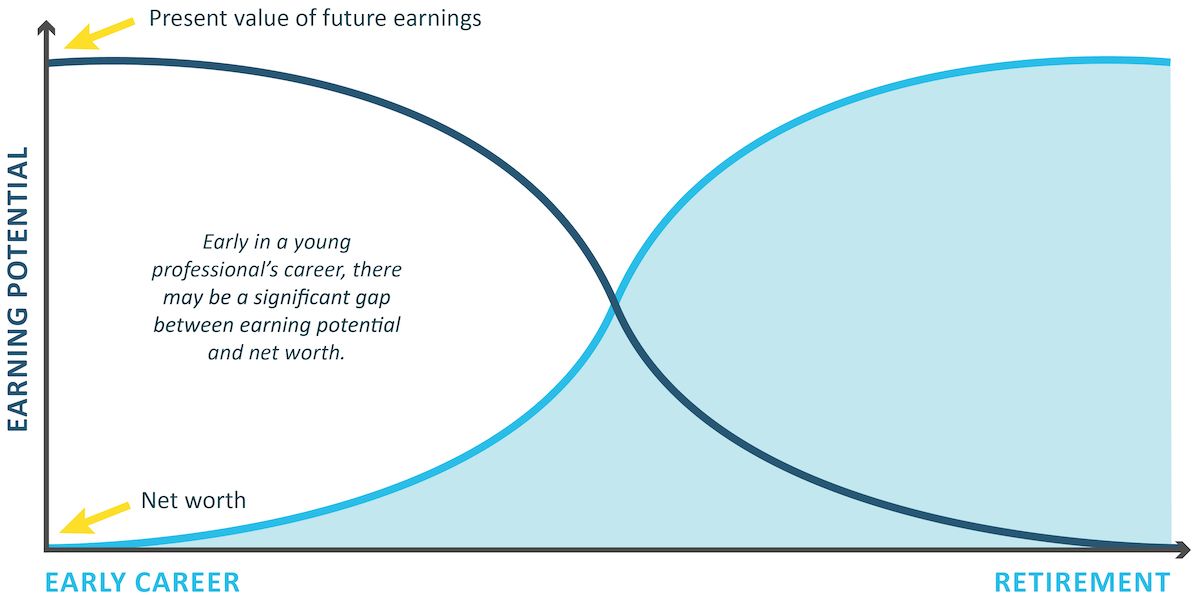

The gap between net worth and earning potential

When young doctors and hospital administrators begin their careers, they may not have saved much and often have significant educational debt. Accordingly, their net worth is usually quite low or even negative.

Now, let’s compare the net worth of young doctors to their future earning potential. At the onset of a doctor’s career, human capital, or the ability to earn and save, is usually at its highest point. Then, over many years, earning potential will decline as one progresses in their profession and approaches retirement. Conversely, as young doctors succeed in their career, their income increases along with their ability to save. This normally results in their net worth increasing – ideally, to a point where they can retire with ample financial resources to enjoy a comfortable retirement. Thus, early in a career, net worth is usually low when the potential to earn and save is at its peak. Over time as wealth builds, these two flip. Protecting your human capital or future earning capacity early in your career is where insurance can help.

When considering insurance coverage, it’s imperative to be aware of this very significant gap between one’s net worth at the beginning of a career versus one’s earning potential.

This chart illustrates how a physician's net worth and present value of future earnings change as they advance from being a new doctor, to establishing a career, to approaching retirement.

© Agili

Recommendations when purchasing additional insurance

Life insurance

With life insurance, there are many rules of thumb to determine how much coverage is needed. However, we recommend a needs analysis based on your specific situation to determine appropriate coverage. A trusted financial adviser can help with this analysis. Here are a few tips to keep in mind when considering life insurance.

First, term life insurance is often a good option for young doctors because it’s usually less expensive than permanent life insurance, allowing you to focus resources on things like saving for retirement as well as paying down debts.

Next, it’s usually more economical and easier to qualify for life insurance when you are young. Down the road, your health status may change and qualifying for coverage later in life may not be as affordable. For this reason, consider convertible term life insurance policies. With a convertible policy, if your health status dramatically deteriorates, you will have the option to convert to a permanent policy during the conversion period, without having to go through a health qualification. Many term policies include this feature, but it is worth checking before you apply.

To save on insurance premiums, you may want to “ladder” term life policies. By “laddering,” we mean to simultaneously purchase several term life policies with varying term dates. For example, when a young doctor or hospital administrator is beginning their career, they may want to purchase three term life policies; one 10-year policy, one 20-year policy, and one 30-year policy. So, early in your life, when your earning potential is highest and living expenses like a mortgage, education, etc., may be at their peak, you have three times the insurance coverage. Over time, as insurance needs decrease, your coverage decreases (every ten years) as do your insurance premiums.

Finally, as your financial situation changes, it is important to periodically review your life insurance needs and coverage. But remember, it is typically much easier to reduce your coverage later in life than it is to add additional life insurance coverage.

Long-term disability insurance

Turning our attention to long-term disability coverage, many people don’t realize that as a young professional one is much more likely to become disabled than to die. That’s why having this coverage in place is so important. Start by understanding what coverage, if any, your employer provides. Most people only get 60% or less of their income covered by long-term disability through their employer. Plus, employer benefits may be taxable, thereby significantly reducing the after-tax benefit amount. If you purchase additional coverage on your own, ensure the premiums are paid with after-tax income so benefits would be tax-free. In addition, young doctors, especially those transitioning from residency to medical practice, should consider purchasing a “future increase option” rider in their long-term disability policy. This rider is an effective way to increase coverage as income rises over time.

Cover the gap between net worth and earning potential

Purchasing additional insurance policies early in a career not only shields doctors and health care professionals from potentially devastating financial consequences but also ensures that they can focus on delivering quality patient care without the looming fear of unforeseen circumstances derailing their careers. By investing in comprehensive insurance coverage early on to cover the gap between current net worth and earning potential, young doctors help fortify their professional foundation and safeguard their future against life’s uncertainties.

Jamie Malone, CFP®, CPA, CFA, is a principal and financial strategist at Agili in Richmond, Virginia, and Bethlehem, Pennsylvania, and is responsible for financial planning as well as financial strategy for clients. Jamie can be reached at [email protected].

Newsletter

Stay informed and empowered with Medical Economics enewsletter, delivering expert insights, financial strategies, practice management tips and technology trends — tailored for today’s physicians.