Article

Getting paid when patients have bare-bones coverage

To cope with the surge in skimpy health insurance policies, adjust your billing and payment procedures. Here's how.

Key Points

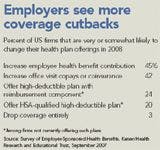

Enrollment in the high-deductible plans alone rose by 1.1 million last year. And a recent survey found that a substantial proportion of US employers expected to scale back on health benefits in 2008 to lower their soaring insurance costs.

As the trend escalates, office-based physicians wonder how it will affect their practice-and their bottom line. Here's what's likely to happen, and what you can do about it.

In 2007, bare-bones plans accounted for 10 to 15 percent of the volume of his company's 300 clients, says Ron Anderson, head of a billing service in southern California. A year earlier, skimpy coverage accounted for just 8 percent.

Kenneth Bowden, a consultant in Pittsfield, MA, forecasts that the 2008 collection ratios at the New England practices he advises will fall by 3 to 5 percent because of difficulties with underinsured patients not paying their bills.

Physicians cite evidence of unfortunate clinical consequences as well. FP John Luehr of the Raiter Clinic in Cloquet, MN, worries that bare-bones plans will impede preventive and chronic care. He says he's already seen diabetic patients with limited coverage skip follow-up visits.

Luehr also has to negotiate with poorly insured patients who need diagnostic and screening tests. "The risks of not getting those tests done need to be discussed," he says, adding that he pushes far harder for crucial care than he would, say, in the case of a bad knee.

Will Sawyer, a solo FP in Cincinnati, sees a similar pattern, with underinsured patients resisting expensive tests. Whenever possible, he suggests less costly alternatives. Thus far, inadequate coverage hasn't gotten in the way of vital care, Sawyer says, "but it has had an impact on less necessary care."

Like many primary care physicians, Sawyer isn't too concerned about financial fallout from bare-bones plans, because his office fees are modest. In fact, he's sometimes glad that patients have to pay out of pocket for his services, because it can be so difficult to collect from local carriers.

In contrast, specialists are well aware that patients in skimpy plans may owe substantial amounts for big-ticket tests or procedures. Knowing that it may be tough to collect from such patients, specialists are more likely to verify benefits and require payments up front. Consultants advise all practices to be aggressive about collecting from poorly insured patients, especially as their numbers grow.

The thinning of insurance will "shine a light on the inadequacies in practices," says Kenneth Hertz, an MGMA consultant based in Alexandria, LA. "Practices that haven't done a good job of collecting copays and deductibles and understanding which of their patients have met their deductibles and which haven't will have a serious problem."